A glance at behavioral science and engagement with applications to insurance

When it comes to offering a new product or a service, engagement with the target customer is key. We want customers to be interested, inspired, motivated and satisfied.

When the service is a health incentive program or an activity-based program, we want customers not only to engage initially in the program or product but also to engage in the healthy behaviors promoted by the program long into the future. The million-dollar question is how do we promote and encourage this engagement?

Unfortunately, there is no silver bullet. But trying to understand human behavior is a good place to start. Concepts from the world of behavioral science can help inform some decisions that need to be made when designing health incentive programs and assist to maximize customer engagement.

In this article we explore two basic concepts in the context of promoting engagement:

-

Loss aversion: Losses loom larger than gains – people are more motivated to avoid losses than achieve gains. This concept can be used in designing components of health incentive programs to encourage certain behaviors.

-

Time preferences: Humans have a tendency to be impatient in short term and more patient in the long term. The discrepancy about what we want now and what we want in the long term poses a challenge in particular when it comes to engaging in healthy behaviors. Short term gratification chosen over long-term results is often the reason why it is not easy to motivate healthy behavior. The challenge is to overcome short-term temptation in favor of long-term goals.

Loss aversion

Consider this initial example to explain loss aversion effect, the concept that losses are more motivating than rewards.

Think about a coin-toss where if tails comes up you lose $100. How much would the winning amount need to be to encourage you to play?

A rational investor is happy with every amount exceeding $100, since the expected value from such an experiment is positive, i.e., in 50% of a series of coin-tosses, they win an amount higher than the one lost in the other half of the tosses.

But most of your fellow human beings would find an amount of around $200 reasonable, which means human beings are more motivated to avoid losses than to achieve gains. The phenomenon called loss-aversion was described by Kahneman and Tversky1 in the late 1970s.

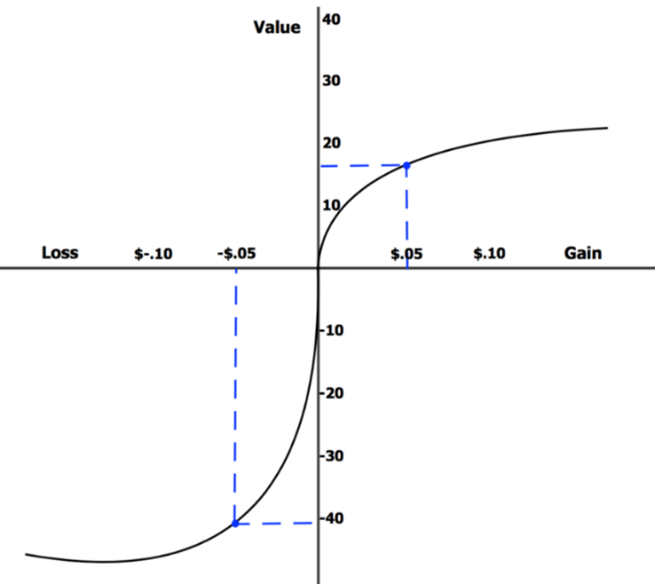

Figure 1: Loss-aversion model

Source: https://en.wikipedia.org/wiki/Loss_aversion#/media/File:Loss_Aversion.png

Figure 1 models this psychological concept mathematically. In absolute figures, a financial gain on the x-axis is perceived less valuable than a loss of the same amount, e.g., a 5-cent gain has a perceived value of less than 20, while losing 5 cents has a negative value of more than -40.

While the basic idea of loss aversion could be applied by including the potential to lose money as well as gain money, other interesting applications are also based on this concept:

Non-financial and financial implications on biological age

At SCOR we use this concept in our Biological Age Model (BAM) products by communicating a biological age (bio age) to people which is based on their physical activity over the course of a week. That bio age score is, by design, not above their physical age.

Even without any financial incentives you can experience a loss of this “age decrease” if the physical activity is not maintained the week after. The reward of getting younger through physical activity is lost if activity is not maintained. This may also be linked to financial incentives, e.g., if a reduced premium or increase sum assured is offered only when the bio age is maintained.

Loss of opportunity for gain

Consider this business case: After signing an insurance contract, the policyholder receives a smartwatch. The smartwatch tracks physical activity, and the policyholder pays premium via monthly installments. If the policyholder fails to meet exercise requirements, he/she is charged with the monthly installment. If the client reaches the monthly activity target, there is no payment needed. More insights to this use case can be found in this study2.

Missing out on a potential win (the lottery concept)

In a study of daily lotteries as motivation in a weight loss program3 participants in the lottery incentive group were eligible for a daily lottery prize with a daily chance of winning of 20%. This means that participants could have a chance to win on a regular basis. Every participant received notifications of the result of the daily lottery, but the prize was only awarded if prior to the draw the participant had achieved a certain weight loss goal.

While winning is not certain, the motivation to achieve the goal is driven by the aversion to losing out on the prize. This design triggers regret aversion through a fear of missing out on the prize in addition to loss aversion. The high winning probability creates a feedback loop, where those that miss out on the reward due to not meeting a goal will be more motivated to ensure they do not face this loss again the next time their name is drawn for a prize.

What other industries do

Understanding and influencing customer behavior is not limited to the insurance industry. In banking applications, loss-framed designs can be used to support customers to reach their saving targets.4

One example is an account where the interest on savings is earned every week, unless a customer did not reach a pre-defined savings goal. This way the customer loses out on interest if he/she doesn’t meet the savings goal.

The messaging is key to whether this design is perceived as a loss as described here. Of course, it could be framed as interest earned if a savings goal is reached, but a potential reward is not as motivating as a potential loss.

Possible limits to the loss-frame

With all the positive effects on engagement and decision making, one should not forget that incentivizing with punishment rather than reward might not be a well-perceived marketing approach. The motivation of loss-aversion is the fear of punishment.

Insurers need to be committed to follow through on this punishment and take this into account when designing the program. Offering opportunities to get back on track after losing out for one week is one way to ensure fairness while leveraging the motivating power of loss aversion. If losses discourage policyholders from continuing in the program, it could look like “cherry-picking” or favoring of good risk by the (re)insurer from a customer’s perspective.

Literature and research highlight the benefits of loss-aversion to influence behavioral changes. The challenge is to implement these learnings in methods which balance this with positive reinforcement of the outcomes.

Time preferences

The concept of time preferences is how we value things we can get today compared to future rewards. Let’s see how hyperbolic discounting effectively models human behavior.

Present bias – our basic human tendency

The present bias tendency to prefer something now rather than later is easy to comprehend. As humans, we tend to be impatient and demand a much better offer in the future to give up a small short-term gain.

Time inconsistent preferences

Under standard economic theory, future rewards are discounted at a constant rate over time. However experimental evidence shows that we tend to be impatient in the short term and more patient in the long term.

Offered a choice between $100 today and $120 in one week, most people choose $100 today. But offered a choice between $100 in one year and $120 in one year and one week, most people choose to wait one week longer for the higher amount. This preference reversal has been demonstrated in multiple experimental studies.5

These types of experiments have revealed preferences are not consistent in time, and alternative models have been proposed to capture differences in short-term and long-term preferences. Laibson6 discusses hyperbolic discounting in the context of choices over time.

Figure 2: Graphical representation of discount functions

Source: Berns GS, Laibson D, Loewenstein G.7

Hyperbolic discounting allows for greater discounting for short time periods than long periods and captures some time inconsistency. Quasi-hyperbolic discounting is a piecewise function that follows a form similar to exponential discounting after the first discount period which reflects extremely high discounting in the short term.

Choices for now and choices for our future selves

Intertemporal choices are decisions made in the present that have consequences for the future. Everyday choices such as what to eat at a meal may have an impact in the future. Most important financial decisions about savings and insurance are made today in anticipation of future outcomes.

Experimental evidence shows differences between choices for present-selves and future-selves. Read & van Leeuwen (1998)8 investigate this with an experiment based on offering office workers a choice of free snack.

Figure 3: Illustration of experiment finding from Read & van Leeuwen (1998)

Source: Read & van Leeuwen8

Most people choose chocolate for now, but more are willing to sign up for the healthy fruit option for next week. This discrepancy between what we want now and what we want in the long term poses a challenge across a wide spectrum of life choices. Short-term gratification chosen over long-term results is often the reason why it is not easy to motivate healthy behavior.

The challenge is to overcome short-term temptation in favor of long-term goals.

Application to health incentive programs

As briefly explained above, BAM offers an insight in the present moment into long-term effects of physical activity. BAM calculates a bio age based on a few parameters such as age, gender, steps, BMI, resting heart rate (RHR), sleep hours and active calories burnt.

The algorithm is based on the long-term impacts of physical activity on health and longevity. The calculated bio age brings those long-term advantages into the present. Each day, activity contributes towards the bio age and measures how much younger the bio age is than actual age.

The goal to reduce bio age is something to achieve now (on a daily basis), and this feedback in the present is much more motivating than the true underlying goal of living a longer, healthier life. Daily feedback, which yields a monthly reward, in turn can become a part of a 24-month “earn your device” program as previously described in the loss-aversion section.

The BAM algorithm is brought to life by the platform it is housed in, such as the Good Life app recently launched in North America. Good Life is a health and wellness engagement app developed by ReMark, a global insurance consultancy that helps insurers worldwide grow sustainably. A subsidiary of SCOR, ReMark has run more than 12,000 campaigns since 1984, reaching more than one billion people with their data intelligence, marketing and technology solutions.

Backed by BAM, Good Life offers its users a variety of immediate and long-term incentives to reduce bio age. Gamification and social techniques such as challenges, leaderboards and friends‘ interactions regularly engage users. SCOR employees in North America participated in a pilot program to test Good Life and BAM during 2020, demonstrating that successful algorithm results are highly dependent on the engagement platform’s ability to motivate and retain users.

"Changing behavior is important, as it can lead to a significant increase in healthy years lived. Understanding the incentive methods that are most impactful is helpful to those trying to change a behavior," said Dr. Bill Rooney, Vice President and Medical Director at SCOR Global Life in the U.S. Dr. Rooney serves on the company's health and wellness team and played a key role in a Good Life pilot.

Conclusion

As insurers move into the space of engaging with customers in new ways, the concepts of behavioral economics can be applied to design health incentives to motivate policyholders to live healthier lives. These two basic concepts of loss aversion and time preference give insights into two important parts of end-customer engagement in health incentive programs and activity-based life insurance products.

There are many more aspects to be considered, and SCOR is committed to applying this research to answer new questions raised as insurance expands its scope. As more of these concepts are tested and validated in the real world over the next couple of years, the insurance industry will increase understanding of our customers, enabling us to develop more customer-centric solutions.

References

1 Daniel Kahneman, Amos Tversky: Prospect Theory: An Analysis of Decision under Risk. In: Econometrica, 1979, Band 47, S. 263–292.

2 Marco Hafner, Jack Pollard, Christian Van Stolk: Incentives and physical activity. An assessment of association between Vitality's Active Rewards with Apple Watch benefit and sustained physical activity improvements. https://www.rand.org/pubs/research_reports/RR2870.html

3 Volpp et al.: Financial Incentive–Based Approaches for Weight Loss: A Randomized Trial, Journal of the American Medical Association, 2008.

4 Roel Wijland, Paul Hansen, Fatima Gardezi: Mobile nudging: Youth engagement with banking apps.

5 Frederick, Shane, et al. “Time Discounting and Time Preference: A Critical Review.” Journal of Economic Literature, vol. 40, no. 2, 2002, pp. 351–401.

6 David Laibson: Golden eggs and hyperbolic discounting. Quarterly Journal of Economics, 1997, 112(2): 443-477.

7 Berns GS, Laibson D, Loewenstein G. Intertemporal choice--toward an integrative framework. Trends Cogn Sci. 2007 Nov;11(11):482-8. doi: 10.1016/j.tics.2007.08.011. Epub 2007 Nov 5. PMID: 17980645.

8 Read & van Leeuwen (1998): Predicting Hunger: The Effects of Appetite and Delay on Choice, Organizational Behavior and Human Decision Processes, 1998, vol. 76, issue 2, 189-205.